‘Beast from the East’ sends Dutch gas price sky-high

After a few quiet years, the Dutch gas market is going through turbulent times. This is mainly due to earthquakes in the Groningen area and the social resistance to gas extraction that followed. Consequently, the Dutch government decided to gradually lower output from the Groningen gas field to zero. However, the majority of Dutch households relies on gas for heating so in cold periods gas supplies are put under substantial pressure. In March 2018, a cold snap originating in Siberia lowered temperatures in the Netherlands. The cold wave, dubbed ‘the Beast from the East’ covered Europe almost entirely. As traders scrambled to secure supplies, the Dutch gas price rocketed. If such an extremely cold period comes along again in the future, the Dutch gas system might not be flexible enough to keep up with the increased demand. In this Energy Market Review, it is questioned whether the Dutch gas system is sufficiently robust so that during extremely cold periods Dutch houses will remain heated. In other words, is the system effective under different market conditions?

The Beast from the East

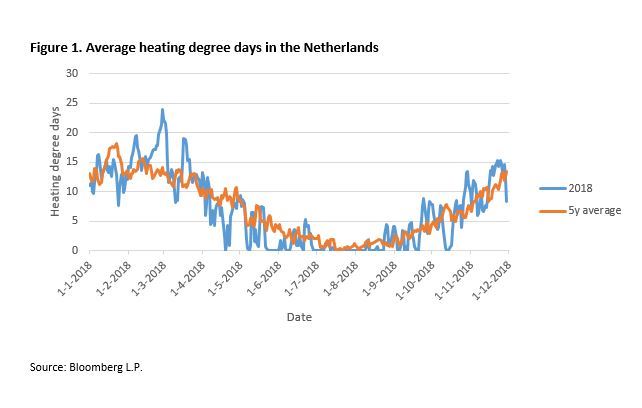

Beginning late February, a cold wave dubbed ‘the Beast from the East’ brought unusually low temperatures to Europe. This large arctic wave covered almost all of Europe, the Netherlands included. Figure 1 shows the average heating degree days. Here, the number of degrees that a day’s average temperature is below 18C° is calculated, since from this point buildings should be heated. For 2018, it shows the highest number for the beginning of March, corresponding to ‘the Beast from the East’. For comparison, a five year average was taken and indeed one can see that it is extraordinary that temperatures reach these levels around March.

The Dutch heating system is currently almost entirely based on the use of natural gas (Mulder & Moraga, 2018) and since people did not want to freeze sitting inside their own homes demand for gas surged. Generally, swing suppliers and gas storages take action in order to meet peak demand. However, here the question arises whether these sources can deliver sufficient gas levels in order meet increased demand.

The Groningen gas field

The Groningen gas field has some specific characteristics which make it a swing supplier. It is relatively easy to extract gas from the Groningen field compared to other gas fields, which is reflected in its lower marginal production costs. Also, the production levels of the Groningen field can be adjusted rather quickly at low costs. This implies that it is perfectly suited for adapting to market conditions and therefore can be named a swing supplier. On extremely cold winter days, like with ‘the Beast from the East‘, they might provide flexibility to the market.

As a consequence of earthquakes in the province of Groningen, the Dutch government decided to impose restrictions on gas extraction in that region. Since seismic activity increased over the years, the cap has been gradually lowered since. Only in case of an abnormal cold year, production is allowed to be slightly higher in order to secure domestic supply (Mulder & Perey, 2018).

The increased incidence and scale of the earthquakes led to strong debates in the Netherlands. The main topic of debate was the trade-off between the national revenues of gas production and security of gas supply on the one hand and the risks and costs beared by the inhabitants of the affected region. Triggered by increasingly intense protests, the Dutch government made a fundamental decision. In March 2018, they decided that the Groningen gas production will come to an end in 2030 (EKZ, 2018). Because the cap of the Groningen field will be lowered gradually, it is less able to act as a swing supplier in the future. Because of this, the role of storages in peak demand periods will likely become increasingly important (Hulshof et al., 2016).

Storage levels

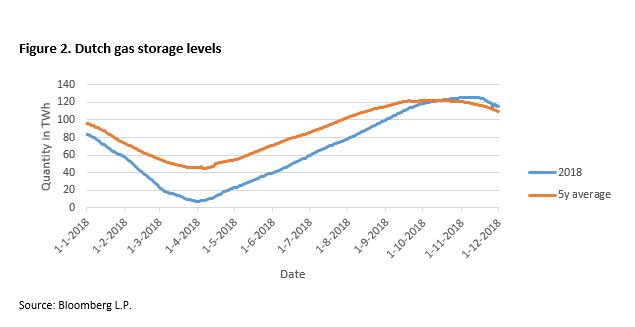

The gas storage levels reached dramatically low levels (7.5TWh) around the time of the ‘Beast from the East’. This is likely the result of increased heating due to the extremely low temperatures. In figure 2, it can be seen that gas storage levels in 2018 in general are lower than the 5 year average. In the beginning of March reserves dropped, which corresponds to the ‘Beast from the East’. This decrease around March is not per se unusual when compared to the five year average, but the decrease is steeper in 2018. This might infer that during an extremely cold period, gas reserves are being used in order to satisfy peak demand.

An alternative would have been to import gas from neighboring countries, but since almost all of Europe was covered by the cold wave every country was faced with the same problem. Therefore, during peak periods this is not really an option. In case of events like ‘the Beast from the East’, a scenario in which gas storages are almost entirely used is not unlikely.

Flexibility might be provided by increasing the gas storage capacity in the Netherlands. Currently, the gas storage ‘Bergermeer’ is the biggest accessible underground gas storage of Western-Europe. It lies close to the city of Alkmaar and is operated by a consortium, including Gazprom. Just like gas extraction, storing gas in empty gas fields is a much debated technique because of the risk of earthquakes. Empty gas and oil fields or salt caverns are suitable for gas storage facilities, but obviously there is a limit to the availability of them. Further possibilities for storing gas are still investigated and developed, but operators must carefully asses the local impact of storing decisions.

Dutch gas price

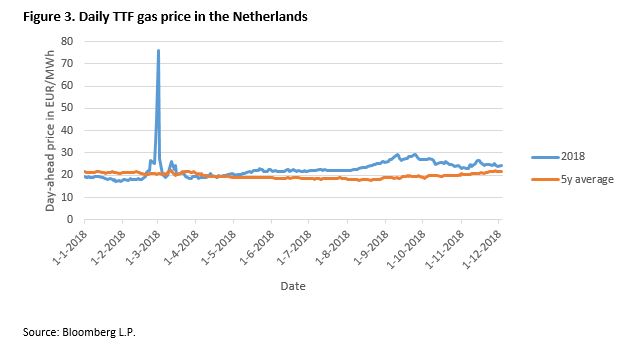

The Dutch gas price spiked to almost 80 EUR/MWh around March 2018, which is also when ‘the Beast from the East‘ covered parts of Europe. The one is inseparable from the other. When comparing it to the five year average, it can be seen that this spike in March is uncommon. Likely, this steep increase in the gas price was a result of the increased demand for gas. Therefore, gas reserves had to be depleted, because otherwise the peak demand could not be satisfied. This corresponds to the decrease in gas reserves around March.

It might also be that prices increased because the Groningen gas field is to a lesser extent able to provide flexibility to the market. In an earlier study, Perey (2018) found that there is no significant effect of a lower cap of the Groningen gas field on Dutch gas prices.

Less flexibility in future Dutch gas system?

The combination of lowering the capacity of the Groningen gas field and the limit to the possibilities of gas extraction make it uncertain whether the future Dutch gas system will be able to meet gas demand in extreme situations such as ‘the Beast from the East‘. The Dutch government plans to rule out gas extraction in the near future, which means the Dutch gas system loses part of its flexibility. This might be compensated by increasing storage capacity, but it also presents significant challenges, like social resistance due to earthquakes.

When new ways for providing flexibility to the market are not found, similar situations to ‘the Beast from the East‘ might be problematic for the Netherlands. It might occur that there is not enough gas to heat all houses. The Dutch government already makes an effort to reduce gas usage. New houses should not be connected to the gas system anymore, which means electrification of the heating sector becomes more important. Mulder & Moraga (2018) provide an interesting view on this in a much debated CEER Policy Paper.

It is difficult to say whether the Dutch gas system is robust enough so that a future beast can be dealt with. Given the limit to both ways of providing flexibility, the Groningen gas field and gas storages, an extreme event might put the Dutch gas system under a lot of pressure. New developments for providing flexibility are required the coming years, but it is not certain what these developments will be exactly. This means the turbulent times on the gas market will probably remain in the coming years.

References

- Hulshof, D., van der Maat, J., & Mulder, M. (2016). Market fundamentals, competition and natural gas prices. Energy Policy(94), 480-491.

- Minister of Economic Affairs and Climate. (2018). Kamerbrief over gaswinning Groningen [letter of government on gas production Groningen]. The Hague.

- Mulder, M., & Moraga, J. (2018). Electrification of heating and transport: a scenario analysis for the Netherlands up to 2050. Groningen: Centre for Energy Economics Research (CEER).

- Mulder, M., & Perey, P. (2018). Gas production and earthquakes in Groningen: reflection on economic and social consequences. Groningen: Centre for Energy Economics Research (CEER).

- Perey, P. (2018). Shake now or extract later; a cost-benefit analysis of lowering the cap on the Groningen gas field, with special attention to earthquakes. MSc thesis, University of Groningen.